SUPPLY: THE PRODUCER RULES

Unit

Overview

In

the marketplace, demand explains the consumer side of purchasing decisions;

supply, on the other hand, relates to the producer. Just as consumers choose what and how much to

purchase, sellers decide what and how much to produce, or supply. The law of supply predicts that producers

will supply more of a good or service if the price goes up and less if the

price goes down. As with demand,

economists use supply schedules and supply curves to illustrate this principle

and to analyze data. They also recognize that several factors other than price

influence supply. Let's see how the

supply side of the marketplace works.

How an

Economist Defines Supply

In a

market system, buyers demand goods and services. In other words, demand focuses on the

consumer. However, if consumers are

going to buy products, someone must create them. It is up to the producer to supply the goods

and services that fulfill the wants and needs of the consumer. For this reason, supply, unlike demand, focuses on the seller. An economist defines supply as the amount of goods and services that are available at

various prices within the marketplace.

Producers try to keep the cost of the factors of production low so that

they can achieve their primary goal, which is to make a profit. They come in all shapes and sizes. Large corporations, small businesses, workers

and individuals who sell products online or at flea markets all qualify as

producers. Do friends or neighbors

sometimes hire you to cut grass, shovel snow or babysit? If so, you are actually providing a service

with the hope of making a profit. This

makes you a producer!

Producers and Consumers at a Produce

Market in Paris, France

![]() Go to Questions 1 through 4.

Go to Questions 1 through 4.

The

Law of Supply

Since

producers are receiving payment for their goods and services, they want to

receive the highest prices for their products.

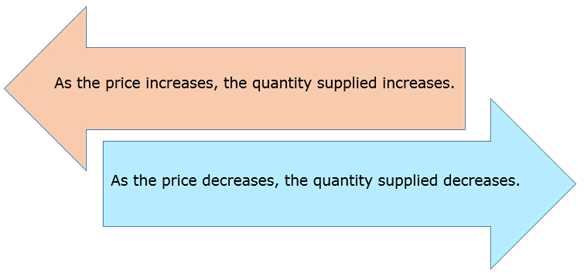

This is the basis for the law of

supply, a principle which states that suppliers offer more products for

sale at higher prices and fewer for sale at lower prices. To make a profit, each individual seller must

decide how much he or she can offer for sale and what price to charge. As long as prices remain high, existing

businesses produce more to earn more.

High prices also provide an incentive,

or reward, for new businesses making similar products to enter the

marketplace. When prices decrease,

existing companies are more likely to offer fewer goods for sale; others may

drop out of the market altogether. In

both cases, the desire for profits

drives the seller's decision-making process.

![]() Go to Questions 5

and 7.

Go to Questions 5

and 7.

Illustrating

the Law of Supply

Rita

is a college student who wants to earn extra money during winter break. She approaches the owner of a local boutique

and asks permission to set up a small coffee bar in front of the store. The owner agrees. As a producer, Rita must decide how much

coffee to make and how much to charge per cup.

According to the law of supply, she wants to sell the most coffee at the

highest price. To accomplish this goal,

Rita thinks like an economist.

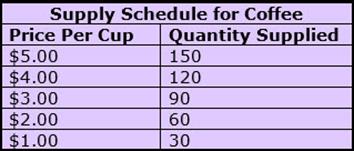

A supply schedule, like a demand

schedule, is a tool used by economists to organize data. It is a listing of the various quantities of

a particular product supplied at all possible prices in the market ceteris

paribus (all other things being equal).

At first glance, it looks just like a demand schedule, but there are

important differences. On a demand

schedule, prices and quantity demanded move in opposite directions. This happens because the demand schedule

supports the law of demand, which states that lower prices increase the

quantity demanded by consumers while higher prices decrease the quantity

demanded. On the supply schedule, price

and quantity supplied move in the same direction. This happens because the supply schedule

supports the law of supply, which states that lower prices decrease the

quantity supplied by sellers while higher prices increase the quantity

supplied. The supply schedule for Rita's coffee business

is pictured below.

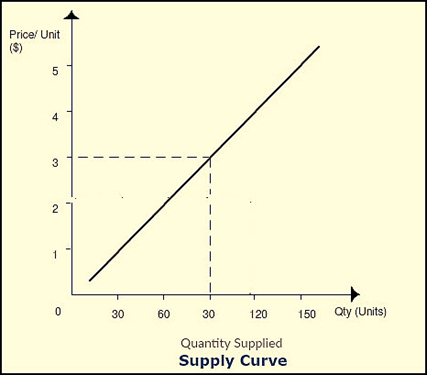

Rita

can also study the relationship between price and quantity supplied by moving

the figures to a graph. This creates a supply curve, which pictures the

quantity supplied at each and every price point present in the market

place. Rita places the lowest possible

price at the bottom of the vertical axis

and the highest possible price at the top.

The horizontal axis shows the

lowest amount of quantity supplied on the left and the highest on the

right. Once Rita plots and connects the

pairs of price and quantity-supplied figures on the graph, the supply curve

appears as pictured below.

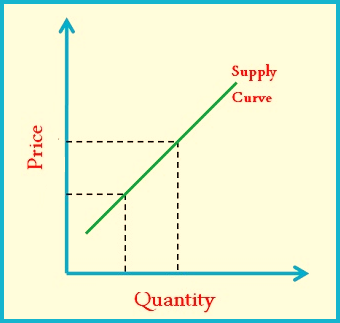

Like

the supply schedule, the supply curve is simply another way to envision the law

of supply. Notice the supply curve

slopes upward to the right as

opposed to the demand curve, which slopes downward to the right. Whether they are analyzing demand or supply,

schedules and curves have similar limitations.

Both assume that all other factors that could affect supply or demand

remain the same. In terms of supply, for

example, the cost of the resources required to make a cup of coffee could

increase, or more sellers could set up coffee shops in the same area. However, if price is the only thing that

changes, we simply move along the curve to a different quantity supplied. As with demand, the curve itself does not

shift in this situation.

![]() Go to Questions 8

through 12.

Go to Questions 8

through 12.

When

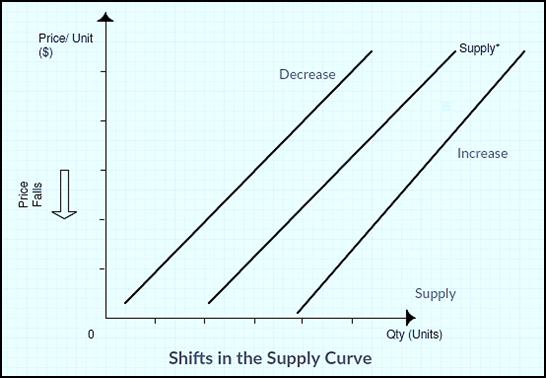

Supply Shifts

Changes

in price result in changes in the quantity

supplied but do not shift the entire supply curve as long as nothing else

comes into play. Sometimes, however, certain

circumstances, or determinants of supply, cause suppliers to offer

different amounts of a particular product at all possible price points in the

market. This results in a change in

supply rather than a change in quantity supplied. It also moves the entire supply curve. When supply increases, the supply curve

shifts to the right; when supply decreases, the supply curve shifts to the

left.

Just

as consumer income, taste and other determinants affect demand at all price

levels, a different set of factors impact supply. These include input costs, technology,

production changes, expectations, number of sellers and government

intervention.

Ø Input costs:

Producers use some of the money that they receive for their goods and

services to pay input costs. Input costs cover a wide range of

expenses, including raw materials, transportation, wages and energy. When a manufacturer is forced to pay more for

inputs, supply falls at all price levels.

This happens because the product becomes more expensive to produce. Therefore, producers offer less, and the

entire supply curve shifts to the left.

A decrease in input costs has the opposite effect. In this instance, supply increases, and the

entire supply curve shifts to the right.

Ø Technology:

Technology is another determinant that influences supply. Updated equipment, innovative industrial

processes and new chemicals often improve efficiency, lower costs and increase

production. This enables producers to

create more goods and shifts the supply curve to the right. Although developments in technology usually

increase supply, it sometimes has the opposite effect. The accompanying upgrades can be expensive

and complicated to install. Replacement

parts for new machinery are often difficult to obtain if the equipment breaks

down. As these costs add up, producers

manufacture less, and the supply curve shifts to the left.

Industrial Robots Moving Products in a German Factory

Ø Production Changes:

Sometimes a company reallocates its resources to produce a different

item that it believes will earn greater profits. This, too, affects supply. For example, a sporting-goods manufacturer

may decide to make fewer footballs and may redirect those same resources to the

production of soccer balls. Therefore, the

number of footballs that the seller is willing to offer in the marketplace

decreases all along the price points of the supply curve. At the same time, the number of soccer balls

that the seller is willing to offer in the marketplace increases throughout the

supply curve.

Ø Expectations:

To achieve their goal of selling at the highest price possible, sellers

often try to anticipate changes in the price of a good or service. These expectations also influence

supply. If producers believe that prices

for certain items will be lower in the future, they may produce and sell as

much as possible immediately. This

results in a short-term increase in supply, and shifts the supply curve to the

right. If, on the other hand, suppliers

expect an eventual increase in prices, they may withhold some of their products

and sell them later. This creates a

temporary decrease in supply, and the supply curve shifts to the left.

Ø Number of sellers:

The number of sellers producing a particular product in the marketplace

is another determinant of supply. As the

amount of firms providing a particular good or service increases, supply

increases. If sellers withdraw from the

market by going out of business or by deciding to make a different product,

less of the good or service is available, and supply, in turn, decreases. Consider this example from the music

industry. Disco music became very

popular in the late 1970s. Some

established groups switched to this style, and new musicians entered the market

to take advantage of potential profits.

This increased the supply of music artists offering disco music. The disco fad, however, did not last

long. Musicians turned to other types of

music, and some left the market altogether.

The supply of disco music and musicians available to play this style

rapidly decreased.

The Disco Craze

of the 1970s

Ø Government Influence:

In the United States, the

government has the authority to affect the supply of many goods and

services. One way in which government

controls supply is through subsidies. A subsidy is a government-issued payment

to encourage or protect a particular business or economic activity. It helps an individual, company or group

lower production costs and remain in the market. American farmers in the

business of providing milk, corn or wheat have sometimes received subsidies to

support their incomes. This enabled them

to continue operating their farms and to remain in the marketplace. While subsidies remain in effect, supplies

increase, and the supply curve for the supported products moves to the right. When the government no longer supports the

subsidy, the supply usually decreases, and the supply curve moves to the left.

Taxes represent another

way in which government affects supply.

Firms view taxes and fees for operating licenses as costs that make

goods and services more expensive to produce.

Therefore, a tax increase on businesses has a negative effect on supply. Tax cuts, on the other hand, have the

opposite impact and increase supply. New

regulations established by law also

influence supply. For example, requiring

certain safety features, such as air bags and back-up cameras, make cars more

expensive to produce. Companies adjust

by manufacturing fewer cars. Because

this happens at every price point in the market, the supply curve shifts to the

left. If regulations are removed or

relaxed, however, the supply curve generally shifts to the right.

![]() Go to Questions 13

through 22.

Go to Questions 13

through 22.

What's

next?

In

the marketplace, buyers, who control demand, and sellers, who control supply,

interact. How can what appears to be

competing interests combine to result in a positive outcome for both sides? What is the key that brings buyers and

sellers together? In the following unit,

you will see what happens when supply meets demand. Before moving on, review the terms found in

Unit 5; then, answer Questions 23 through 30.

![]() Go to Questions 22

through 30.

Go to Questions 22

through 30.

|

| Unit 5 Main Points Worksheet |

| Unit 5 Law of Supply Worksheet |

| Unit 5 Determinants of Supply Worksheet |